There has been a lot of debate around the power of fandom in the creative sector over the years.

Back in 2008, Kevin Kelly, former editor of Wired, wrote the 1,000 True Fans essay, which suggested that a creator on the internet only needs 1,000 superfans to earn a living from their art.

In 2020, Li Jin, co-founder of Variant Fund, proposed that a creator only needs 100 true fans to make a living from their work.

One thing is for sure, so-called ‘superfans’, who are willing to spend more than the average fan on merchandise, music and other content, are a lucrative target audience for artists and their teams.

And as dominant music industry players start pushing for alternative streaming payout models, such as Universal Music Group‘s proposed “artist-centric” model, it’s the superfan category that could rewrite the music industry’s revenue story in years to come.

Speaking on UMG’s Q1 earnings call, Michael Nash, UMG’s EVP and Chief Digital Officer, indicated that an “artist-centric” model would look to increase revenue flow from “superfans” – or in other words, individuals who are willing to pay more for subscriptions in exchange for additional content.

“Our consumer research says that among [music streaming] subscribers, about 30% are superfans of one or more of our artists,” said Nash.

He added: “How does that relate to artist-centric? When you start to focus on the artist-fan relationship, these high-value relationships are driving the economic model of the platform, so you [can begin] segmenting around high-intent, high-integrity, artist-fan relationships.”

Recent stats published by US market monitor Luminate have shed more light on the extent of such ‘high-value relationships’ between artists and fans in the United States.

According to Luminate’s mid-year music report, which you can read in full here, 15% of the general population in the US are ‘superfans’.

Luminate breaks down what it meant to be a superfan, explaining that for its report, its methodology defines a superfan as, “a music listener aged 13+ who engages with an artist and their content in multiple ways, from streaming to social media to purchasing physical music or merch items to attending live shows”.

‘Superfans’, according to Luminate’s report, spend 80% more on music each month versus the average US-based music listener. Additionally, physical music buyers of formats such as vinyl, CDs or cassette tapes, are more than twice as likely (+128%) to be music superfans.

Millennial music listeners, meanwhile, spend over 22% more and Gen Z music listeners spend over 13% more on music compared to the average US music listener, according to Luminate’s report.

Luminate also points to the growth in Direct-to-Consumer (D2C) sales to highlight the buying power of the superfan category.

According to Luminate, D2C sales of music from artists’ stores were up over 20% in H1, with D2C vinyl sales up 26% YoY in H1, to 3.6 million copies. Meanwhile, 1.7 million CDs were sold Direct-to-Consumer in the first half of the year, an increase of 15% YoY (see below).

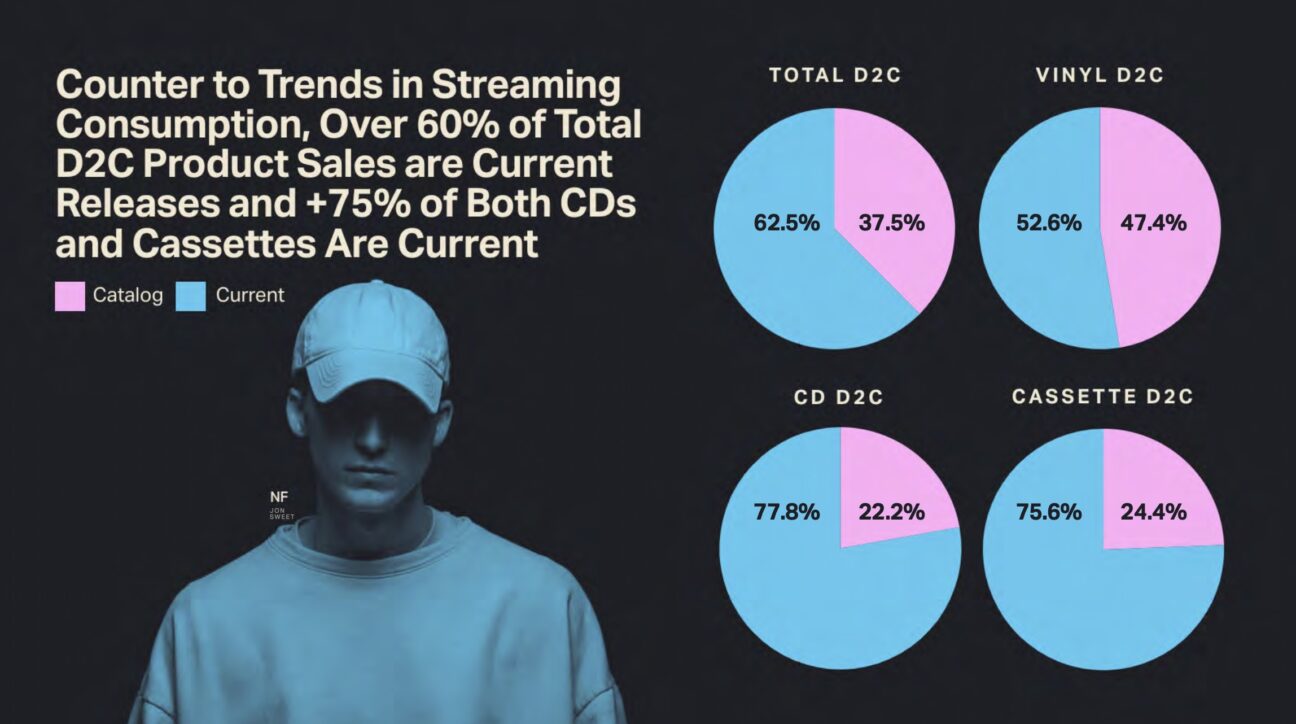

A surprising stat highlighted by Luminate is that 62.5% of total D2C product sales are of ‘current’ releases.

As noted by Luminate in the diagram below, this is counter to the trend in streaming consumption.

According to Luminate’s midyear report, of the 538.9 million album-sale-equivalent (TAC) units recorded in H1 2023, 72.8% (392.1 million) were registered as ‘Catalog music’.

‘Current’ Music’s share of Total Album Consumption in the United States in the first six months of 2023 was 27.2%, or 146.8 million TAC units.

Luminate defines ‘Current’ as anything released in the 18 months prior to it getting streamed/downloaded/purchased. Anything older than 18 months when it’s streamed/downloaded/purchased is defined as ‘Catalog’.

Breaking down superfan activity by genre, Luminate reports that K-Pop fans spend 75% more money on music per month than the average music listener in the US.

According to Luminate, K-Pop fans are also over 69% more likely than fans of major genres including pop, R&B, hip-hop and rock, to buy an album on vinyl in the next 12 months.

Afropop and Afrobeats fans, meanwhile, spend 121% more money on music categories per month than the average US-based music listener, according to Luminate.

EDM fans spend over 63% more money on music categories per month than the average U.S. music listener.

The potential financial impact of the superfan category was also recently highlighted by Goldman Sachs.

In Goldman’s latest Music In The Air report, it claimed that if 20% of paid streaming subscribers today could be categorized as ‘superfans’ and, furthermore, if these ‘superfans’ were willing to spend double what a non-superfan spends on digital music each year, it implies a $4.2 billion (currently untapped) annual revenue opportunity for the record industry.

As explained in our recent analysis of Goldman’s report, that $4.2 billion figure represents a ‘Total Addressable Market’ (TAM).

Goldman Sachs also models out a scenario whereby things start off much slower, with just 10% of ‘superfans’ (i.e. 2% of total subscribers) paying double the price for their streaming service in the first year following the launch of a ‘superfan’-orientated product.

However, if this percentage of addressable ‘superfans’ paying for extra access could gradually be bumped up to 70% by 2030, says Goldman, it could end up bringing in an extra $4 billion-plus to the recorded music industry annually.