Credit: TDC Photography/ShutterstockRound Hill Music's UK-listed fund is especially strong in the rock genre – owning copyrights by bands like Bush (pictured)

MBW Reacts is a series of analytical commentaries from Music Business Worldwide written in response to major recent entertainment events or news stories. MBW Reacts is supported by JKBX, a technology platform that offers consumers access to music royalties as an asset class.

You’ll have seen the name New Mountain Capitalcrop up a few times on MBW of late – thanks to its interest in potentially acquiring the biggest PRO in the world by value, Broadcast Music Inc (BMI).

Yet as we’ve mentioned before, NMC already has a significant ownership interest in the music business… one that’s attracted a few rays of the spotlight over the past week.

Seventeen months ago, NMC acquired a majority stake in Citrin Cooperman, described in the takeover PR as “a top full-service advisory, tax and assurance firm in the United States”.

NMC swooped for Citrin Cooperman just three months after the latter firm had confirmed its own acquisition of Massarsky Consulting – the music-industry-specialist valuation firm run by Barry Massarsky and Nari Matsuura.

So dominant is Massarsky/Citrin in the world of music business valuations that, across the course of 2022, it valued music assets cumulatively worth more than $6.5 billion.

After announcing Concord’s proposal to the markets on Friday (September 8), RHM made available to its investors a number of illuminating documents.

One of those documents, reviewed by MBW, is a thorough breakdown of Citrin Cooperman’s valuation of Round Hill Music Royalty Fund on the date of September 8 – the same day Concord’s offer was made public.

The Citrin document makes for interesting reading – shedding light, amongst other things, on the multiple of net revenues that Concord has offered for RHM (which runs both a publishing company and a record company – so we’re talking ‘net publisher share’ plus ‘net label share’, here).

Round Hill’s ‘independent valuer’ says it’s worth over $650m – at a multiple of 19.56X of NPS

Citrin Cooperman (CC), described as Round Hill’s ‘independent valuer’, valued two separate assets on September 8 in relation to the Concord offer:

The first was Round Hill Music Royalty Fund Ltd (RHM) itself, which CC valued at USD $558.21 million;

Additionally, CC valued RHM’s ownership stake in Carlin Music – a publisher with songs made famous by Elvis Presley and others – at $96.53 million.

RHM became the owner of a 29.14% stake in Carlin Music in May 2021. (The remainder of Carlin is owned by private funds controlled by Round Hill’s New York-based investor management company.)

If Concord’s bid for RHM is accepted by the latter company’s shareholders, Concord will take control of both RHM and of RHM’s 29.14% stake in Carlin.

In total, then, CC gives RHM (including its stake in Carlin) a ‘fair value’ of USD $654.75 million.

The key calculation in Citrin Cooperman’s valuation of RHM on September 8, 2023

CC has based this valuation, it reveals in its workings, on a multiple of 19.56X annual net revenue for RHM‘s assets (including that Carlin stake).

CC says this 19.56X multiple is in line with the average multiple that was paid for publishing catalogs in a number of comparable transactions that took place in H2 2022 and H1 2023 involving other Citrin Cooperman clients.

We can therefore work backwards from CC’s $654.75 millionvaluation of RHM – and its stated 19.56Xmultiple of that valuation – to work out the implied annual net revenue of RHM’s assets.

Here goes: A valuation of RHM’s assets of$654.75 million/ a stated multiple from Citrin Cooperman of 19.56X= an estimated annual net revenue of RHM’s assets of $33.47 million.

Understanding Concord’s offer

Obviously enough, then, Concord isn’t offering the full ‘fair value’ of Round Hill as set out by Citrin Cooperman.

Concord’s offer – $468.8 million– is close to $200 million smaller than CC’s valuation of RHM’s assets ($654.75 million).

So what gives?

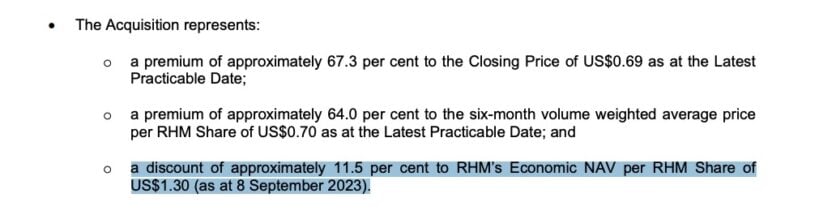

First thing to know: Round Hill’s letter to shareholders last week confirmed Concord’s offer came in at an official discount of 11.5% vs. the valuation that Citrin Cooperman put on RHM (plus its stake in Carlin) on September 8.

The relevant part of Round Hill’s letter to shareholders RE: the discount applied to Round Hill’s valuation from Citrin Cooperman (-11.5%)

Said11.5% discount on the Citrin Cooperman valuation of USD $654.75 million would give Round Hill a ‘gross asset value’ (GAV) in Concord’s acquisition bid of USD $579.45 million.

This ‘GAV’ number is important when it comes to playing with the true multiple number paid here, so bear with us.

Remember that Citrin Cooperman’s valuation of Round Hill’s assets was based on a multiple of 19.56X and, therefore, an annual net revenue of $33.47 million?

The GAV above ($579.45m), with that 11.5%discount factored in, would mean Concord just offered an effective multiple of 17.31X on the implied annual net revenue of Round Hill’s assets.

(Quick math to explain: A 17.31 multiple X annual net revenue of $33.47 million = that GAV in Concord’s offer of $579.45 million).

We have a bit more work to do, though.

That’s because, obviously enough, applying an 11.5% discounton Citrin Cooperman’s valuation of RHM’s assets (i.e. taking us down to the ‘GAV’ of $579.45 million) doesn’t get us down to the actual amount offered by Concord ($468.8 million).

There is a difference between these two numbers of ~$110 million.

This seems simple to explain: It’s pretty much all due to RHM’s debt pile.

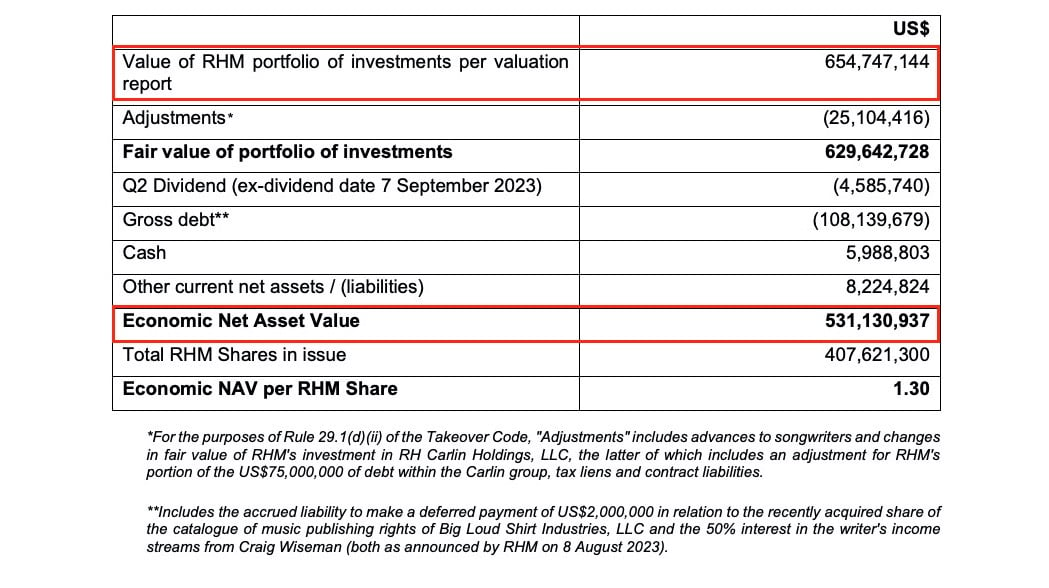

According to the letter from RHM to its shareholders sent September 8, setting out Concord’s offer, RHM had $108.15 million in gross debt on its books as of September 8, 2023.

Due to this, and a further $25 million in negative ‘adjustments’ (including RHM’s portion of Carlin’s separate $75 million debt pile), the ‘Economic Net Asset Value’ of Round Hill sat at USD $531.1 million as of September 8.

(See below: ‘Economic Net Asset Value’ is Citrin Cooperman’s valuation of RHM’s assets minus their net liabilities… including all that debt.)

It was this ‘Economic Net Asset Value’ that Concord applied an 11.5% discount to in its monetary offer, bringing $531.1 million down to a $468.8 million bid.

A slide from the Round Hill / Concord shareholder offer letter showing how Citrin Cooperman’s valuation of RHM’s assets is reduced by liabilities (mainly debt) to calculate ‘Economic Net Asset Value’

Did Concord get a bargain? Time will tell.

What’s really interesting about the multiples knocking around on this page is that, from one angle, they might look conservative.

Here’s why.

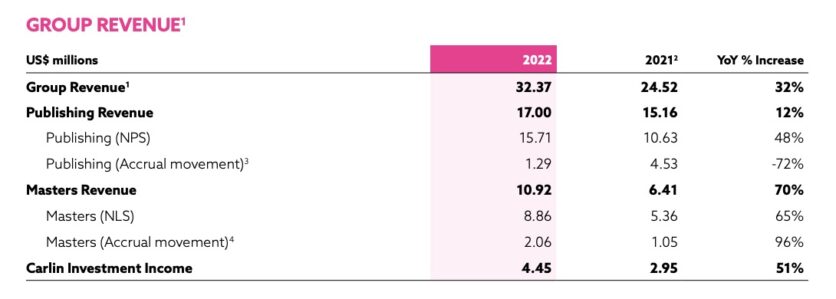

Round Hill’s FY 2022 group revenues weighed in at USD $32.37 million – made up of $17 million in publishing revenues, plus $10.92 million in recorded music revenues, and a further $4.45 million in income from the Carlin investment.

That $32.37 million in 2022 annual net revenue fits pretty closely with the 19.56Xmultiple that Citrin Cooperman applied to compute its latest valuation of RHM’s assets (remember; CC’s multiple published on September 8 implied an annual net revenue for RHM’s assets of $33.47 million).

However, there’s another take here.

In July this year, RHM issued a single-sheet Q1 trading update to its investors.

It showed that in the three months to end of March 2023, RHM generated $10.18 million in quarterly net revenue – up 94% YoY.

(This $10.18m figure was helped by a $1.32m ‘accrual movement’ in publishing revenue that appears to have been driven by a bump in US streaming service payments thanks to the Copyright Royalty Board’s recent rulings.)

Round Hill’s calendar Q1 2023 revenues, showing that $10.18 million net revenue figure

It would be a bold – some might say foolhardy – bidder who would base an acquisition offer on a single quarter’s performance. Especially when that quarter saw a near-doubling in an M&A target’s net revenues.

Then again, there were signs that Q1 wasn’t necessarily a one-off from Round Hill: The firm said its125% YoY rise in ‘net label share’ (NLS) revenues in the quarter – up by around $2 million YoY – was primarily down to “[recent] catalog acquisitions including Alice In Chains, David Coverdale and Dennis Elliott”.

Meanwhile, the ever-reliable income of the classic Carlin catalog (including 100,000 songs performed by artists like Elvis, Johnny Cash, Aretha Franklin, and Ella Fitzgerald) saw a 225% YoYspike in the quarter (possibly because of a lucrative sync or two).

You see where this is leading: If RHM could repeat that $10.18 million Q1 revenue in each of the subsequent three quarters of 2023, it would be looking at annual net revenue this year of some $40.7 million.

Remember that all-important ‘GAV’ figure used for Concord’s bid for the RHM assets: $579.45 million.

If RHM’s assets could achieve an annual revenue of $40.7 million in 2023 (at this stage, a bullish but not outlandish forecast), Concord would surely be happy – having paid an effective 14.2Xmultiple of this annual revenue to buy the RHM portfolio.

(Admittedly not taken into account in this suggestion: The potential for declining/’decaying’ revenues from particular RHM copyrights in the future, as well as expiring ownership of copyrights… both of which Citrin Cooperman says it takes into account when figuring out its valuations.)

What’s Concord buying, exactly?

It’s worth briefly looking at what might make Round Hill’s UK fund attractive to a buyer like Concord – especially in terms of genre.

Earlier this summer, Concord CEO, Bob Valentine, told MBW that one of his company’s priorities in the months ahead was gaining more of a foothold in frontline recorded music, in genres such as pop.

That’s as maybe, but another priority for Concord – if the Round Hill deal goes through – will also be rock.

According to RHM’s 2022 results, more than half the firm’s revenues (and therefore the company’s ‘fair market’ valuation), some 56%, came from rock recordings and songs last year.

That genre percentage was up on a 45% share in 2021.

Round Hill’s latest annual report explains that its performance in the rock genre in 2022 was driven by “hits from some of the biggest rock legends in the world including Alice In Chains, Bush, Supertramp and The Offspring“.

It added: “Rock fans are known for their enduring loyalty, resulting in predictable and steady purchase patterns and music consumption habits, translating into income characteristics.

“These facts are borne out in recent independent market studies. The Luminate U.S. Year-End Music Report for 2022 shows that total on-demand streaming in the US for Rock grew by 14.2% year-on-year from 2021 to 2022; whilst in the UK – the world’s third largest music market – Rock was the leading genre in 2022 for album sales for the fifth consecutive year, according to… record industry trade body BPI.”

Right now, shareholders of Round Hill Music’s UK-listed fund seem generally pleased with Concord’s bid – following a bumpy road on the stock market since RHM’s IPO in November 2020.

In reaction to Concord’s bid (being made as Alchemy Copyrights, LLC), Caspar Rock, Chief Investment Officer at Cazenove Capital – which owns about 10% of Round Hill and 6% of Hipgnosis Songs Fund – has given the deal the thumbs up.

According to the Financial Times, Rock said: “Alchemy is paying a full and fair price for Round Hill Music, which validates the thesis that there are buyers for music rights and the independent valuation [of RHM] is about right.”