Credit: Shutterstock/Ben HoudijkSza'sSOS was one of the best-performing albums in the US in H1 2023

US market monitor Luminate (formerly MRC Data / Nielsen Music) has been the source of a number of head-turning stats about the modern music business this year.

In April, for example, Luminate revealed that on-demand music audio streams across the world crossed the one trillion mark in Q1 – marking the first year in history that milestone has been reached in just three months.

We also learned, via Luminate, that an average of 120,000 ISRCs (i.e. new music audio files) were added to music streaming services – across audio and video platforms – per day in Q1 2023.

Now the company has published its midyear report for H1 2023, which you can download here. It reveals H1 music consumption stats from the US and globally, and highlights listening trends across the business.

Here are the headline stats:

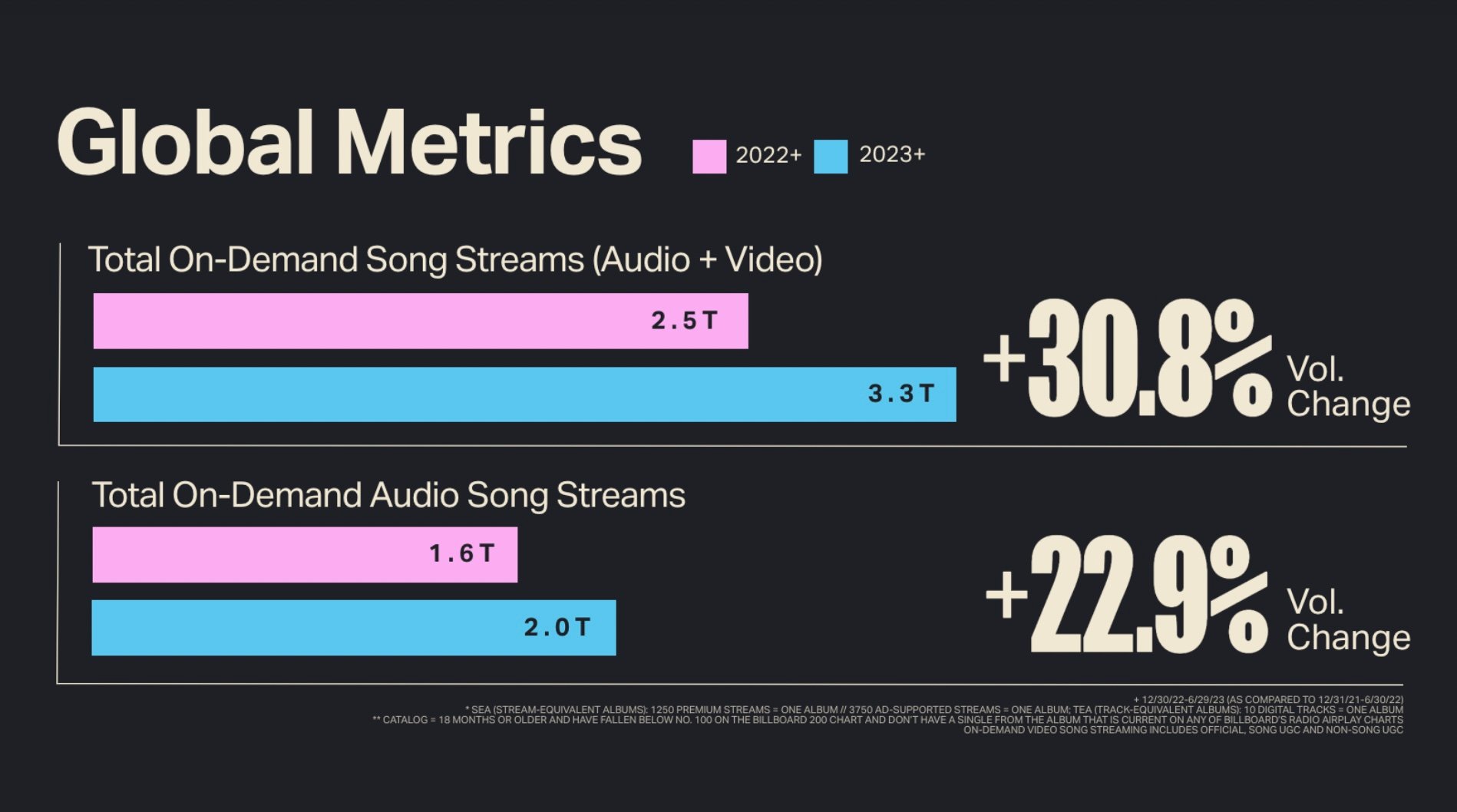

Globally, according to Luminate, total on-demand song streams (Audio + Video) grew 30.8% in H1 2023 to reach 3.3 trillion in total, compared to 2.5 trillion on-demand song streams in H1 2022 (see below).

Total on-demand audio song streams globally rose 22.9% YoY to 2 trillion, according to Luminate’s report.

In the world’s largest recorded music market, the United States, on-demand audio streams grew 13.5% to reach 616.5 billion.

On-demand song streams, meanwhile (including audio and video) grew 15% YoY to 713.5 billion streams (see below).

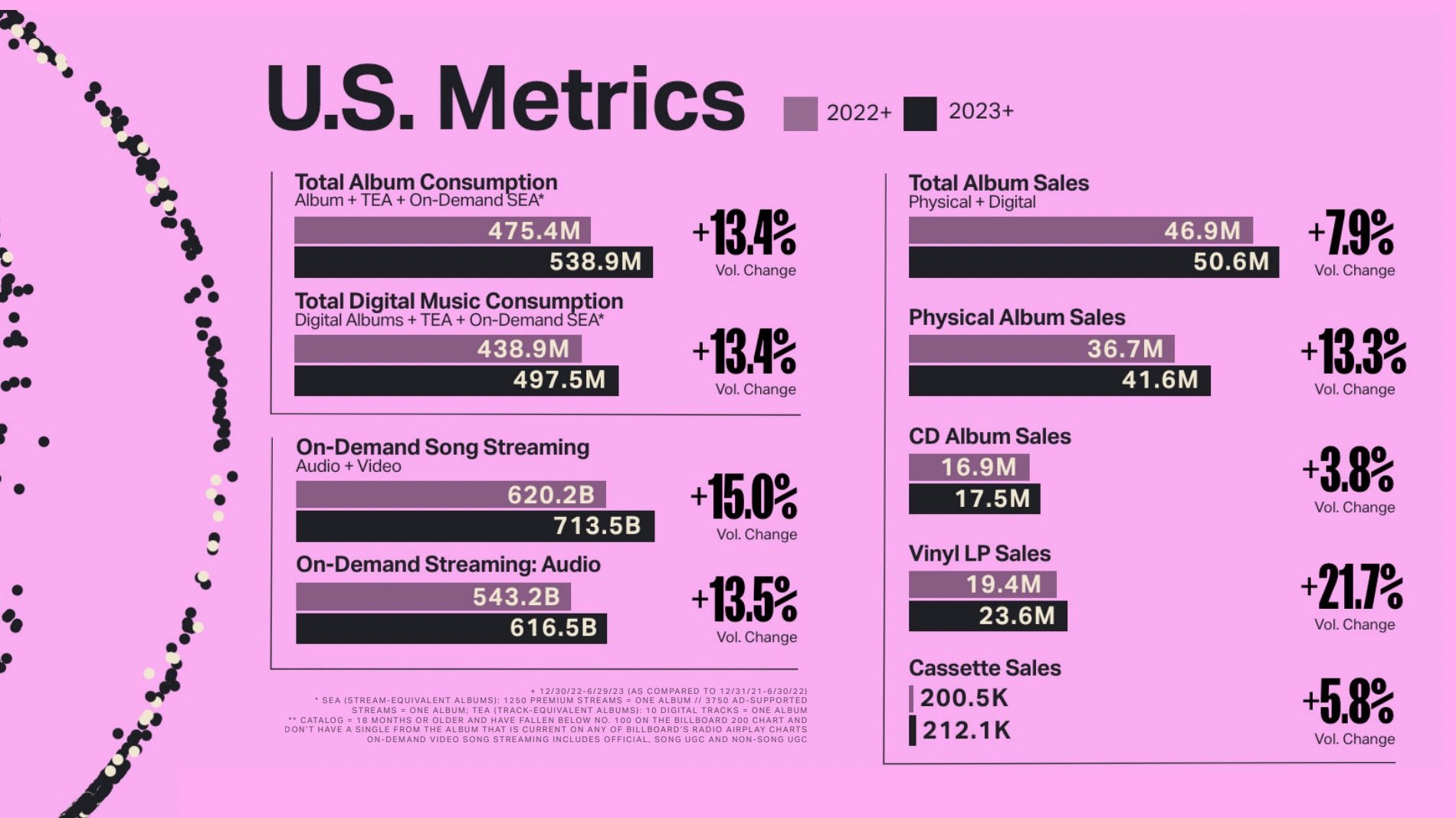

Total Album Consumption (TAC) of all music in the United States in H1 rose 13.4% to 538.9 million album-sale-equivalent units in H1 2023 (see above).

Luminate’s ‘Total Album Consumption’ (TAC) metric combines all on-demand track streams, plus all track downloads, plus all album sales on digital and physical formats.

The formula for ‘TAC’ equates 1,250 premium streams, or 3,750 ad-supported streams, to one album ‘sale’ .

It also equates 10 digital track purchases/downloads to one album ‘sale’.

Alongside the release of the report, Luminate also announced the launch of its new international music data offering, which provides country-level streaming data for 47 new countries in the company’s database.

The new offering joins the company’s current US and Canada-level data sets, along with its global (inclusive of 40+ ex-US and Canada markets) streaming and digital song sales data set that launched in 2018.

Maarten de Boer

“The first half of 2023 is defined by more empowered Super Fans with a growing hunger to support their favorite artists.”

Rob Jonas, Luminate

Speaking on the release of the report and the new international data offering, Rob Jonas, CEO, Luminate, said: “Verified data is essential to understand the who, where, and why of shifts in cultural trends, especially given the ever-growing global nature of the music industry and the continued disruption and growth of music engagement at large.

“As laid out in Luminate’s Midyear Music Report released today, the story of music in the first half of 2023 is defined by more empowered superfans with a growing hunger to support their favorite artists, more engagement with non-English music in the U.S., and more content being uploaded on a daily basis, which creates more opportunities and challenges.

“The key word here is “more,” which leads to the need for a more focused and insights-fueled understanding of worldwide music listener habits. We are especially looking forward to Luminate’s new international data offering expanding the entertainment industry’s understanding of existing and forthcoming trends outside of the US market in the coming quarters.”

Here are five standout stats and takeaways from Luminate’s latest midyear report…

1. Catalog’s share of US music consumption increased in H1.. but only slightly

Luminate defines ‘Current’ as anything released in the 18 months prior to it getting streamed/downloaded/purchased.

Anything older than 18 months when it’s streamed/downloaded/purchased is defined as ‘Catalog’.

According to Luminate’s midyear report, of the 538.9 million album-sale-equivalent (TAC) units recorded in H1 2023, 392.1 million, or 72.8%, were registered as ‘Catalog music’.

This means that ‘Current’ Music’s share of Total Album Consumption in the United States in the first half of 2023 was 27.2%, or 146.8 million TAC units.

While the popularity of ‘Current’ music grew by 11.8% in the US in 2022, the popularity of ‘Catalog’ music grew 13.9%, according to Luminate’s report (see below).

This margin of growth between ‘Catalog’ and ‘Current’ music wasn’t as large in the first half of 2023 as it was in H1 2022, when ‘Total Album Consumption’ of ‘Current’ recorded music in the United States actually fell1.4% in volume versus the equivalent metric from the same period of 2021.

‘Current’ music’s 11.8% rise in TAC consumption volume in H1 2023, versus the equivalent metric from the same period of 2022 (H1), was driven by dominant new releases, including the likes of Morgan Wallen’s One Thing At A Time, SZA’s SOS and Taylor Swift’s Midnights.

In spite of the 11.8% rise, ‘Current’ Music’s share of Total Album Consumption in the United States in the first half of 2023 was still less than it was in the first of 2022, when it had a 27.6% share.

2. The volume of new track uploads to DSPs may have hit a peak in Q1…

In May, we reported, citing Luminate data, that an average of 120,000 ISRCs (i.e. new music audio files) were being added to music streaming services – across audio and video platforms – per day in Q1 2023.

That figure worked out to a total of 10.08 million new tracks uploaded to the likes of Spotify, YouTube Music and other music streaming services in the first three months of the year alone, according to Luminate.

We pointed out that if the number of average daily new track uploads continues at the same rate of 120,000 per day for the rest of the year, by the end of 2023, over 43 million new tracks will have been uploaded to Spotify and other music streaming services this year.

According to Luminate’s new midyear report for H1 2023, the upload rate has now slowed down.

Including ISRC ingestion activity from Q2, across the whole of H1 2023, the average number of ISRCs (i.e. new music audio files) being added to music streaming services was 112,000, with 20.2 million uploads in total during the period.

Does this indicate that the vast number of daily uploads to music streaming services has peaked? We’ll need to wait for Luminate’s full-year report to paint a broader picture of this trend.

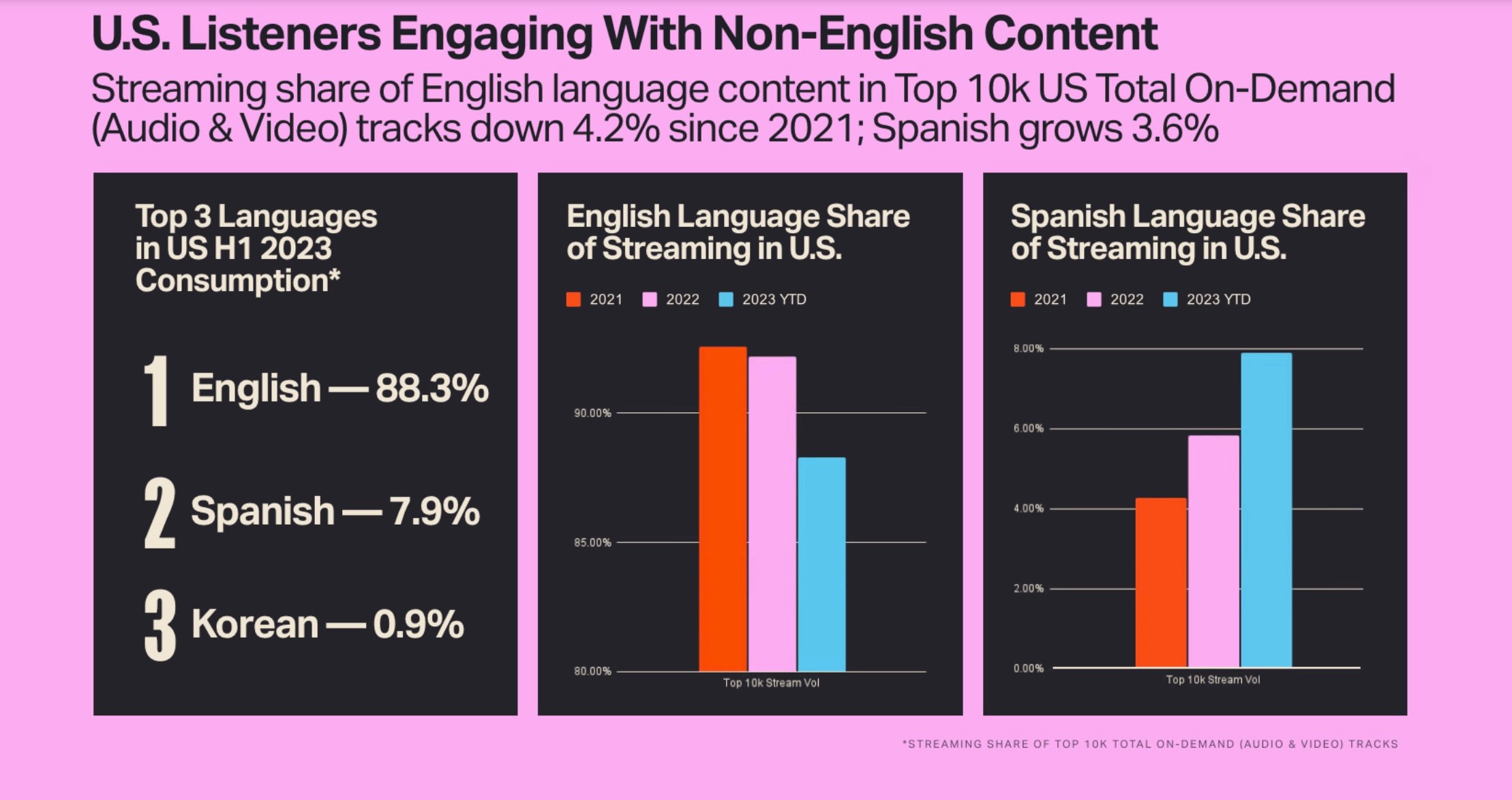

3. English language music is losing streaming share in the US, and globally.

Amidst the growing popularity of non-English language music from the likes of Korea and Latin America, English language music’s share of total on-demand audio streams is shrinking in the United States.

According to Luminate’s mid-year report, in H1, the streaming share of English language content in the Top 10,000 US Total on-demand (Audio & Video) tracks was down 4.2% since 2021.

Spanish language music’s streaming share of the Top 10,000 US on-demand (Audio & Video) tracks, on the other hand, has grown 3.6% in the same time frame.

In the US, English language music’s streaming share of the Top 10,000 US on-demand was 88.3% in H1. Spanish language music had a 7.9% share of the equivalent metric.

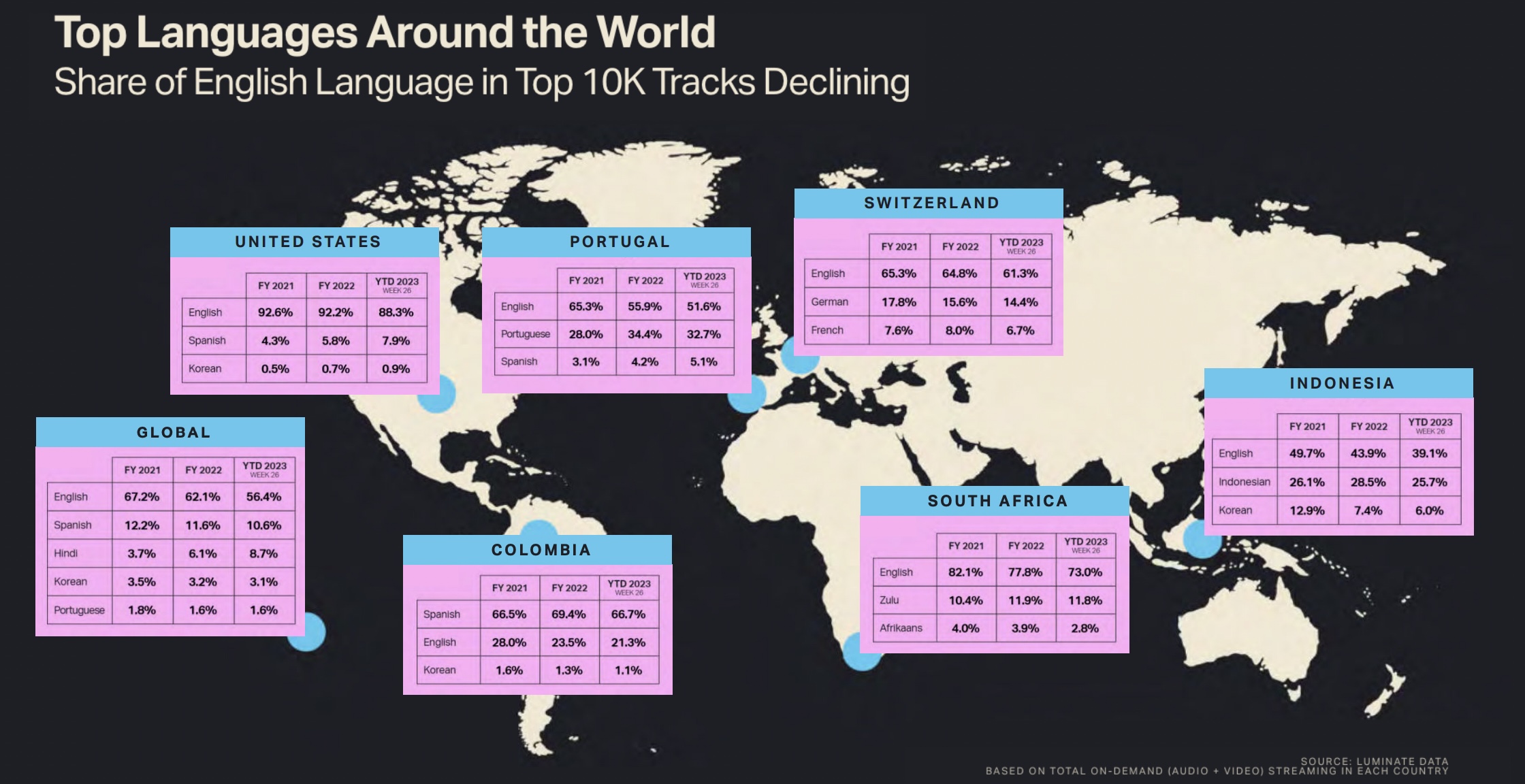

English language music’s declining share of the Top 10,000 tracks on streaming services is not just a US trend, but a global one (see below).

According to Luminate, English language music’s share of the Top 10,000 tracks on streaming services globally in 2022 was 62.1% versus 67.2% in 2021.

In the first half of 2023, English language music’s share of the Top 10,000 Total on-demand (Audio & Video) tracks fell to 56.4%.

Luminate points to a similar trend in multiple markets worldwide, including Portugal, South Africa, Indonesia, Colombia and Switzerland. English language music’s share of the Top 10,000 Total on-demand (Audio & Video) tracks in each of these markets fell in 2022 versus 2021, and again in H1 2023.

4. Regional Mexican music is seeing significant growth in the US, and Don’t forget about Afrobeats…

Luminate offers Snapshots of three specific genres that are seeing growth globally, including Regional Mexican Music, Afrobeats and J-Pop.

MBW has previously written about the explosion of Regional Mexican Music taking place alongside the wider Latin Music boom.

According to Luminate, US on-demand audio streaming YTD of Regional Mexican music was up 50% in H1 versus the same period in 2022.

In the first half of the year, Regional Mexican music generated 10.4 billion On-Demand Audio Streams in the US.

One of the stand-out acts cited by Luminate includes Elsabon Armado, who generated 1.6 billion On-Demand Audio Streams globally in the first half of the year and 766 million in the US.

Afrobeats, meanwhile, generated 2.5 billion On-Demand Audio Streams in the US by the mid-year point according to Luminate’s new report, up 34% versus the equivalent period in 2022.

Burna Boy, one of the world’s biggest Afrobeats stars, generated 1.1 billion Global On-Demand Audio Streams in the first half of the year, and 255.8 million in the US.

J-Pop generated 662.4 million On-Demand Audio Streams in the US in the first half of 2023, which was up 29.6% versus 2022.

5. 15% of the general population of the United States are ‘superfans’

Last, but not least, Luminate offers a comprehensive overview of ‘superfan’ trends in the music industry.

According to Luminate’s mid-year report, 15% of the general population of the United States are superfans.

‘Superfans’, according to Luminate’s report, spend 80% more on music each month versus the average US-based music listener, and physical music buyers (Vinyl/CDs/Cassettes) are more than twice as likely (+128%) to be music super fans.

Breaking down superfan activity by genre, Luminate reports that K-Pop fans spend 75% more money on music per month than the average music listener in the US. Afropop and Afrobeats fans, meanwhile, spend 121% more money on music categories per month than the average US-based music listener

One thing is for sure, superfans are a lucrative target audience, and as dominant music industry players, such as Universal Music Group, start pushing for more “artist-centric” streaming models, it’s the superfan category that could make a gigantic difference to the record industry’s coffers in years to come.

Speaking on UMG’s Q1 earnings call, Michael Nash, UMG’s EVP and Chief Digital Officer, indicated that “artist-centric” would look to increase revenue flow from “superfans” – or in other words, individuals who are willing to pay more for subscriptions in exchange for additional content.

“Our consumer research says that among [music streaming] subscribers, about 30% are superfans of one or more of our artists,” said Nash, adding: “How does that relate to artist-centric? When you start to focus on the artist-fan relationship, these high-value relationships are driving the economic model of the platform, so you [can begin] segmenting around high-intent, high-integrity, artist-fan relationships.”

Goldman Sachs, in its recent latest Music In The Air report, claimed that if 20% of paid streaming subscribers today could be categorized as ‘superfans’ and if these ‘superfans’ were willing to spend double what a non-superfan spends on digital music each year, it implies a $4.2 billion (currently untapped) annual revenue opportunity for the record industry.

As explained in our recent analysis of Goldman’s report, that $4.2 billion figure represents a ‘Total Addressable Market’ (TAM). Goldman also models out a scenario whereby things start off much slower, with just 10% of ‘superfans’ (i.e. 2% of total subscribers) paying double the price for their streaming service in the first year following the launch of a ‘superfan’-orientated product.

However, if this percentage of addressable ‘superfans’ paying for extra access could gradually be bumped up to 70% by 2030, says Goldman, it could end up bringing in an extra $4 billion-plus to the recorded music industry annually.Music Business Worldwide