The MBW Review offers our take on some of the music biz’s biggest recent goings-on. This time, we investigate how much money the record labels are spending on ‘A&R’ – and what this means for their bottom lines as each year passes. The MBW Review is supported by Instrumental.

Every couple of years, global music trade body, IFPI, releases figures which show just how much money its record label members – both independent and major – are cumulatively spending on artists.

This year, these figures have arrived via a new microsite, which shows that total worldwide spending by record companies on artists – across both ‘A&R’ and marketing/promotion – hit $5.8bn in 2017.

That $5.8bn was up nearly 30% on the previously published figure, for 2015 ($4.5bn) and included a $4.1bn spend on A&R, alongside $1.7bn artist marketing costs.

MBW has drilled down further into the changing spending patterns of the record industry (via IFPI statistics published since 2008) and noticed a striking macro trend: the amount of money labels are paying to sign and develop artists is mushrooming, while increasingly eating into these companies’ potential profits.

First, an important clarification about the IFPI data above: the ‘A&R’ figure includes obvious artist expenditure such as money required for recording studio time, as well as remixes and other costs related to making music.

However, MBW has clarified with the IFPI that ‘A&R’, in this case, constitutes ‘total artist expenditure’ – ie. it also includes advances paid in order to sign acts, as well as some royalty money handed over to new talent.

It is no secret that major record companies now struggle to ink deals with artists in accordance with the contracts these companies were once able to get signed – both in terms of the duration for which the label will own/control the rights, and the percentage of digital royalties they will pay out.

For example, instead of signing away their master copyrights in perpetuity, it is becoming increasingly common for today’s acts to sign shorter-term licensing deals with major record companies. And instead of agreeing to a 15%-20% royalty rate, today’s artists are more likely to demand anywhere up to 50% (or, in some cases, even more).

Plus, with more money flowing around the market generally, advances paid to ‘hot’ artists are anecdotally cranking up as labels behave in a more fiscally competitive manner.

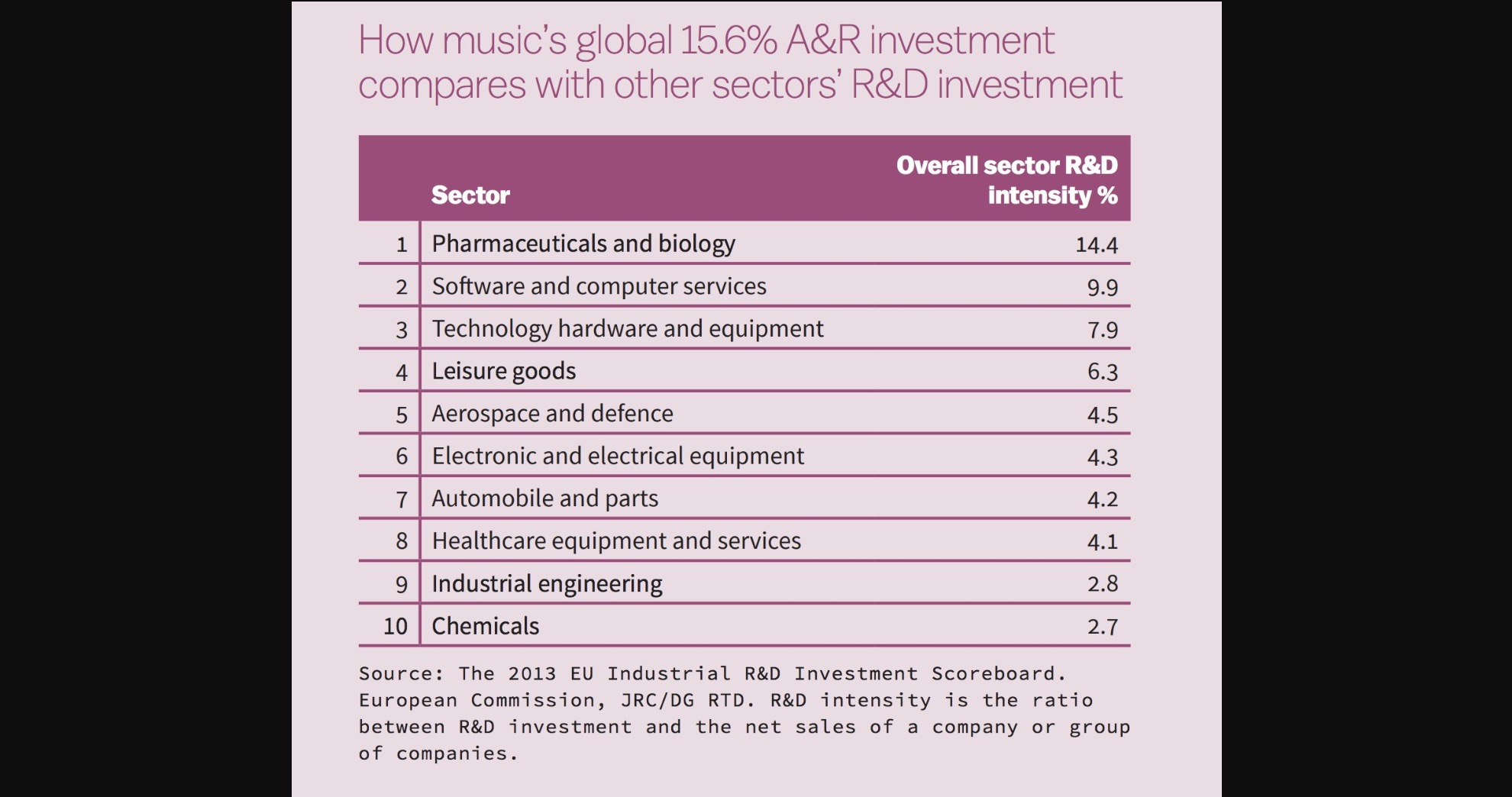

Over the past decade, the IFPI’s published statistics regarding record industry investment in artists have always come with a very clear underlying message: the record industry spends more on ‘A&R’ (ie. the signing and developing of artists), as a percentage of its overall annual revenues, than any other industry spends on ‘R&D’ (the closest equivalent category of investment in other business types).

This, presumably, was a useful lobbying tool for the IFPI when it came to arguing for the fiscal generosity and/or economic movement of the record industry.

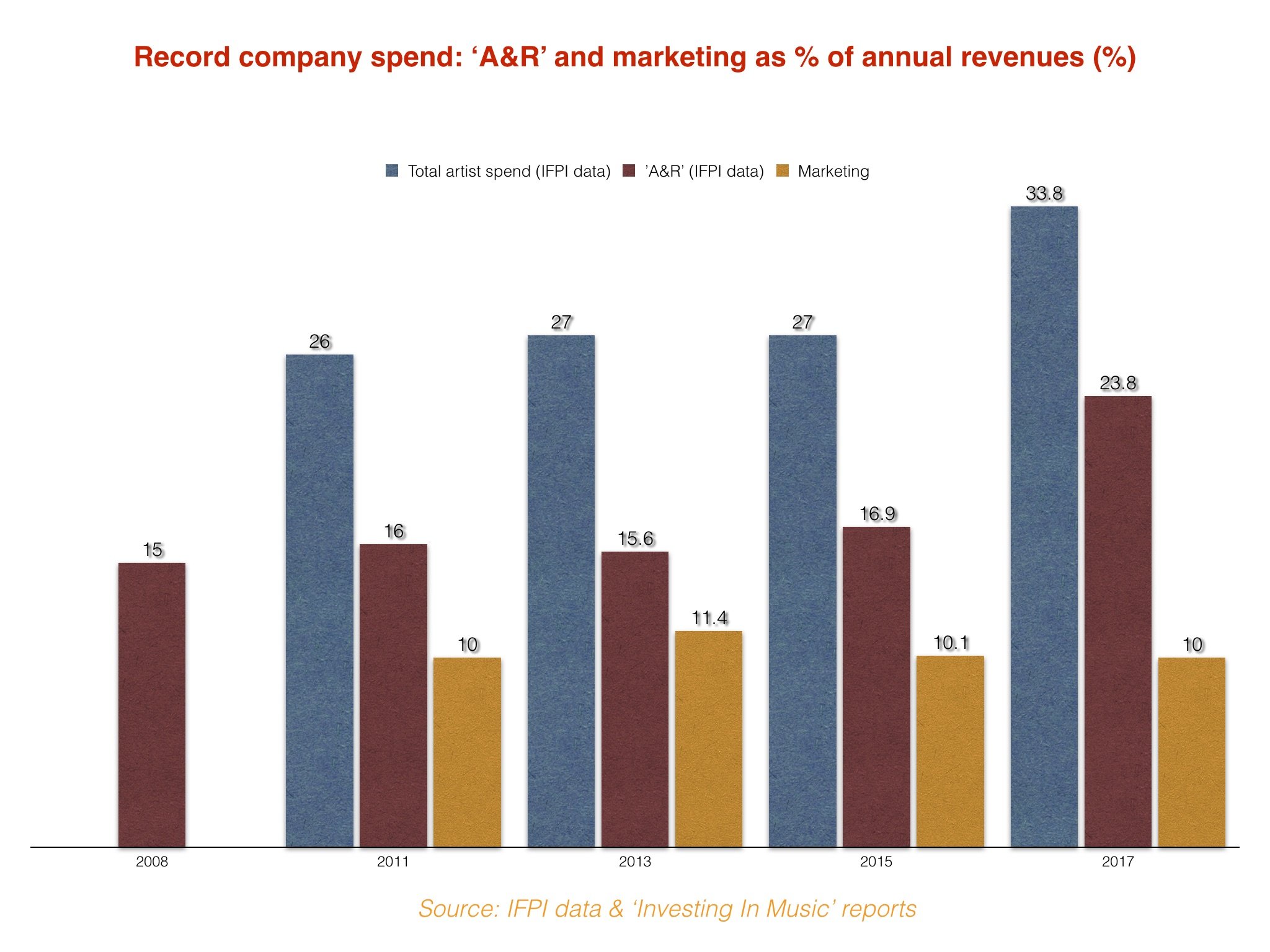

We saw it in IFPI reports regarding 2008, 2011, 2013 and 2015 data – most of which were labelled ‘Investing In Music’. See below for an example from IFPI’s 2013 report.

According to IFPI data, in the five years between 2008 and 2013, this annual number (the % of total industry revenues devoured by its A&R spend) remained fairly consistent at around 16%.

Yet in 2015, the figure jumped – up to 16.9%, as revealed by that year’s ‘Investing In Music’ report.

In its set of numbers for 2017, IFPI doesn’t reveal the A&R-spend-as-a-%-of-industry-sales figure, but it does give us enough information to make an estimate.

If total artist spend (‘A&R’ plus marketing) of $5.8bn claimed 33.8% of industry revenues in 2017 – as confirmed by IFPI’s microsite – then it follows that a $4.1bn A&R spend was equivalent to approximately 23.8% of overall industry revenues.

(All of the ‘A&R’ and ‘Total artist spend’ numbers below, aside from the 2017 ‘A&R’ figure, have previously been published by the IFPI. ‘Marketing’ is simply the remaining % figure in each case, as only these two categories make up IFPI’s total spend number. MBW hasn’t been able to confirm IFPI’s ‘Total artist spend’ or ‘Marketing’ numbers for 2008, so these are left blank.)

As you can see above, since 2013, the record industry has managed to tame its spend on artist marketing and promotion to around 10% of its annual revenues.

This chimes with the idea that the user data afforded to record companies in the age of streaming and social media has enabled these companies to spend their promotional dollars in a more targeted way.

(It should also be noted that this 10% rate has been maintained despite – according to an RIAA-commissioned report – the number of artists signed by US major labels rising 12% to 658 in 2017.)

However, it’s a very different story when it comes to the percentage of annual sales that the record industry has earmarked to sign, develop and pay talent in the modern age – which reached close to a quarter (23.8%) in 2017.

Before you start feeling too sorry for the labels, of course, we should remember that they’re paying out a bigger % of a bigger revenue pie: in the US, for example, record industry wholesale revenues hit $6.6bn in 2018, up on $5.2bn two years prior.

Yet the fresh IFPI statistics published here tell us something very important: as artist power in label negotiations continues to grow, and the industry’s resultant deals get ever more competitive, the record business’s new-age economics are really starting to show.

[Pictured: Ed Sheeran, the world’s biggest recorded music artist in 2017, according to IFPI stats.]