Harry Styles' Fine Line was the UK's second biggest album across all formats in 2020, behind Lewis Capaldi's debut LP

The MBW Review is where we aim our microscope towards some of the music biz’s biggest recent goings-on. This time, we run the most recent market numbers out of the UK to see what’s going on in the world’s third largest territory for recorded music. The MBW Review is supported by Instrumental.

Annual growth in music streaming volume in the United Kingdom was widely expected to slow down in 2020. Instead, driven by the pandemic lockdown, it sped up – in a big way.

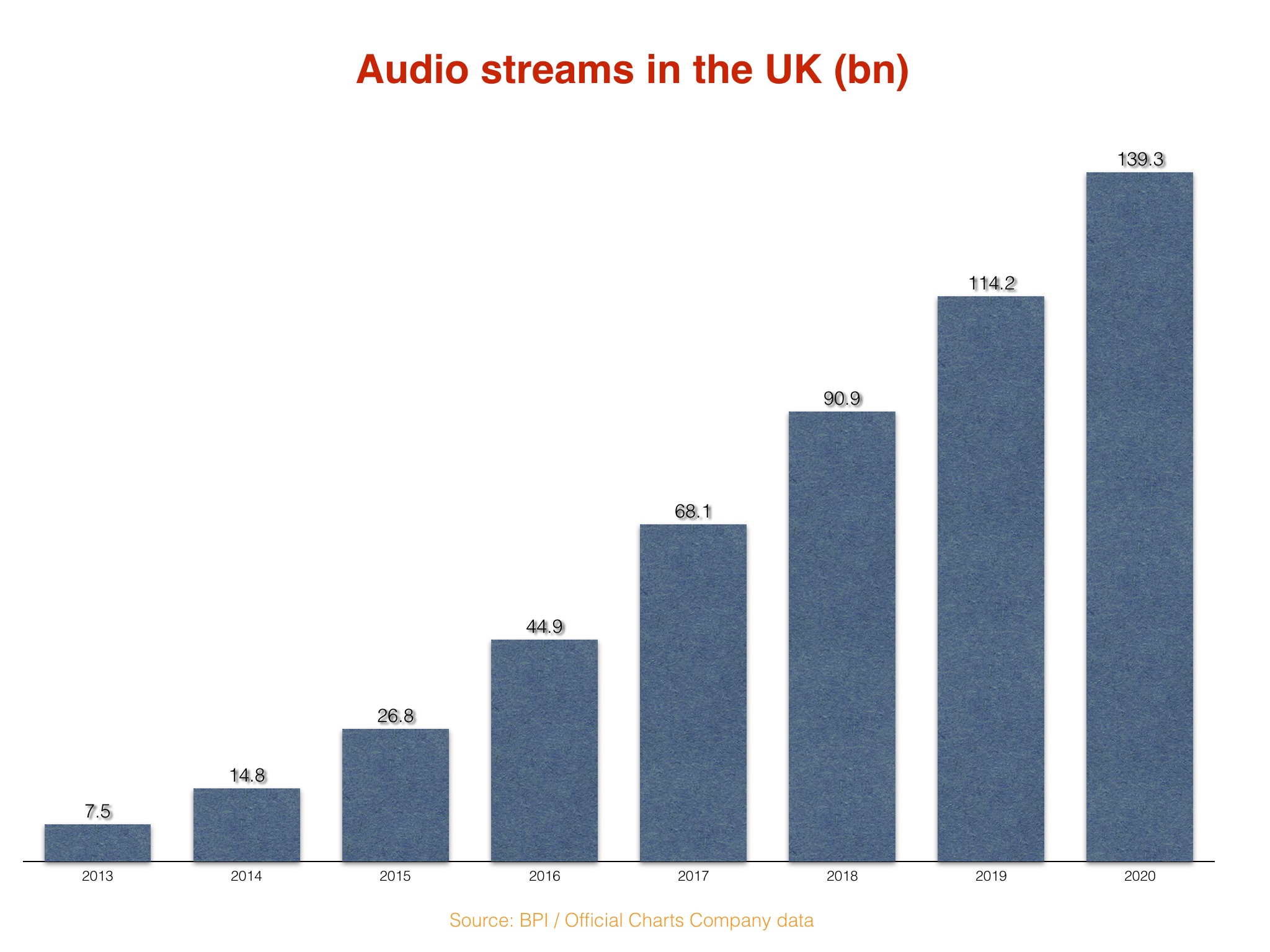

According to new BPI statistics analyzed by Music Business Worldwide, the UK played host to 139.3bn audio streams across the 12 months of last year.

That was up by 25.1bn on the UK’s total audio streaming volume in 2019, which stood at 114.2bn.

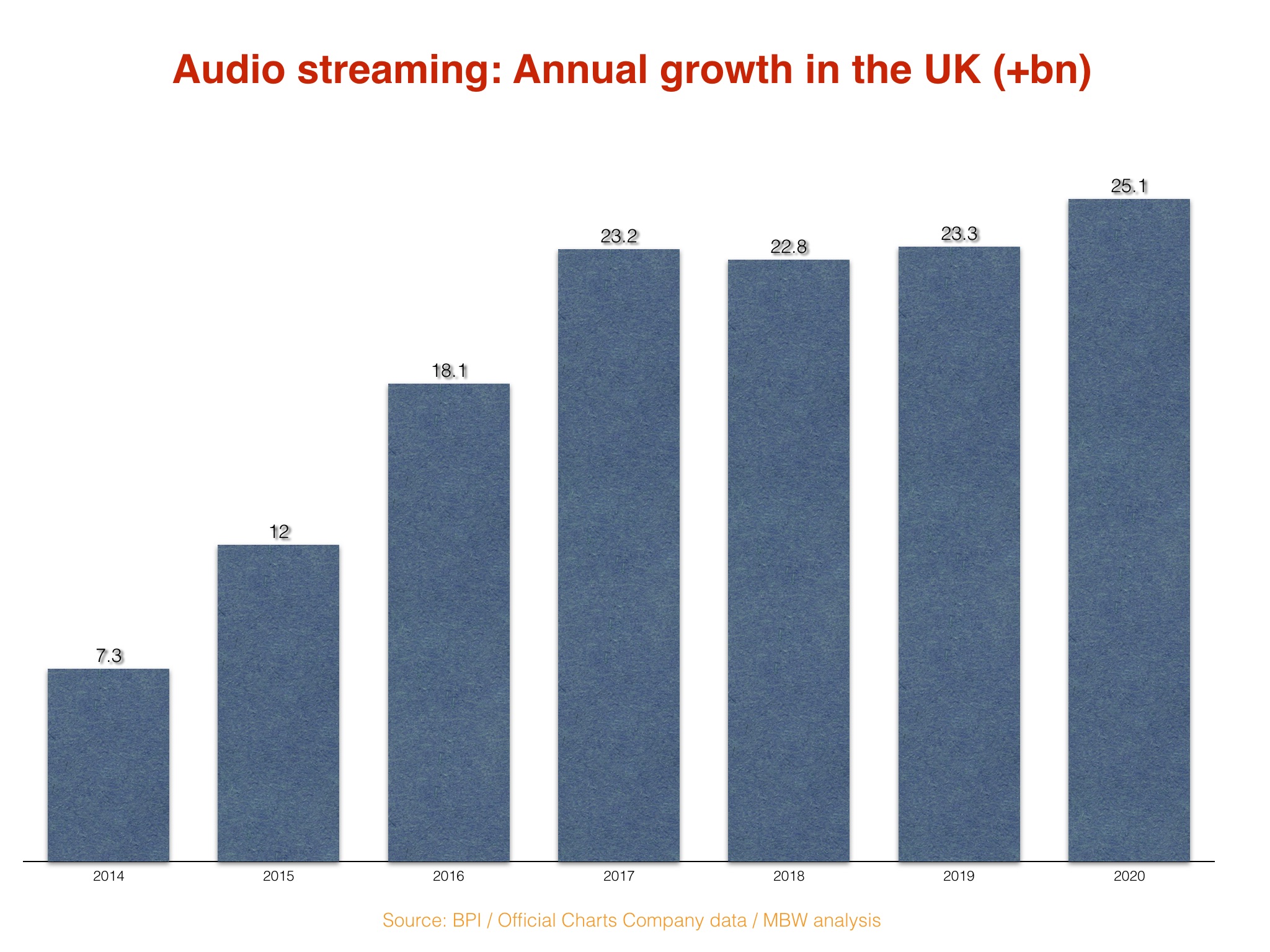

2020, therefore, saw the UK’s biggest ever annual growth in audio streaming volume.

The reason many believed the UK’s total audio streaming volume growth would slow in 2020 is simple: it’s a mature streaming market, having welcomed Spotify‘s back in 2009, two years before the US.

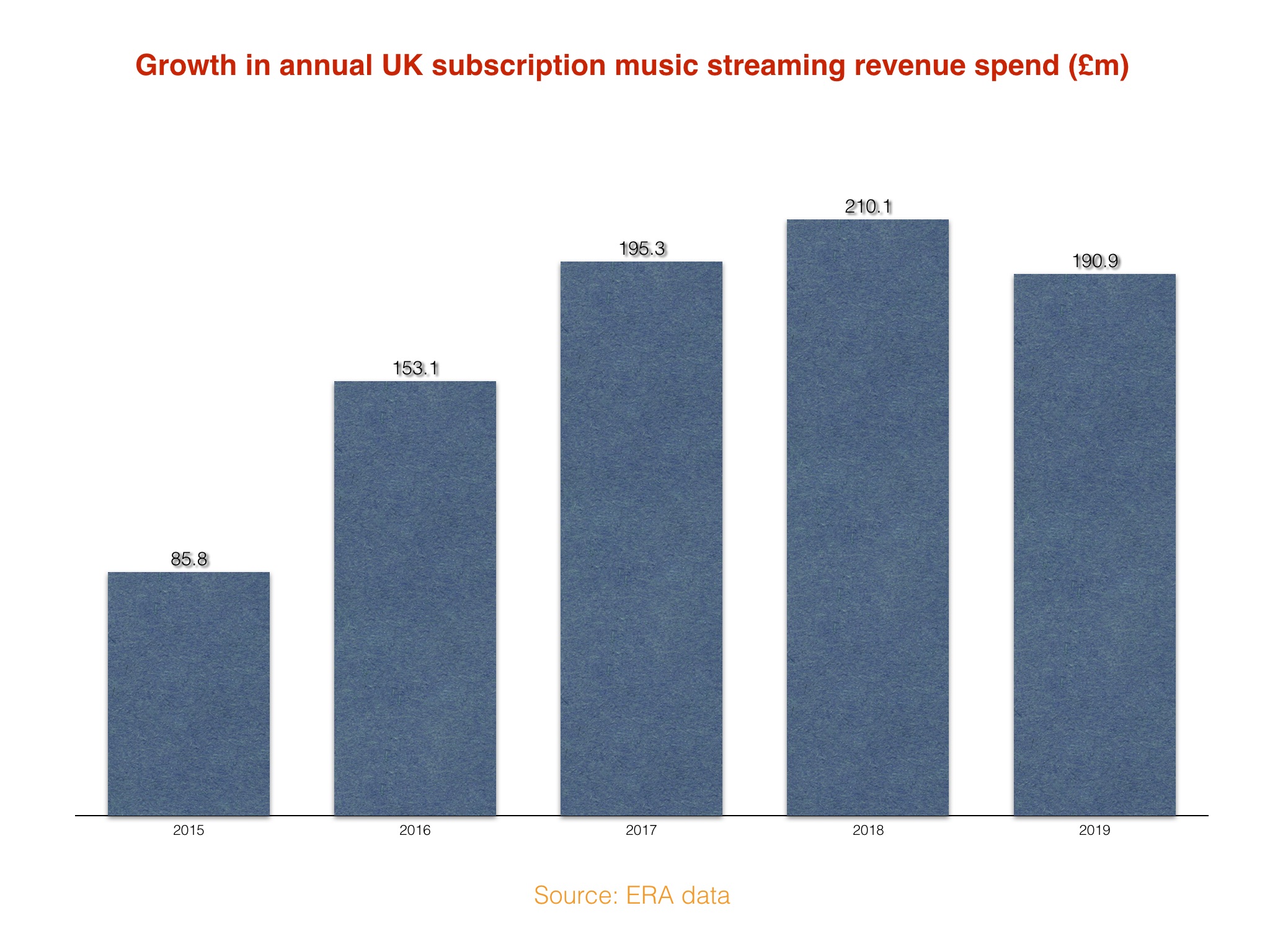

As a result, annual growth in streaming subscription revenue has been slowing in the UK of late: in 2019 – according to stats from the Entertainment Retailers Association (ERA) – the UK’s total spend on streaming subscriptions grew by £190.9m year-on-year, which was down on the £210.1m annual growth seen in 2018, and down on the £195.3m growth seen in 2017.

We’re currently awaiting new annual streaming revenue statistics for 2020 from ERA – which will allow us to see if this decline in growth continued last year.

The BPI, in contrast, offers us data about the volume of streaming in the UK, the world’s third largest recorded music market. Its figures cover both paid-for and ad-supported streaming activity in the territory.

And, in this context, the UK music industry can allow itself a smidgen of celebration (indoors, please, and strictly no mixing of households).

MBW’s analysis shows that the 25.1bn growth in total audio streams seen in the UK in 2020 was significantly larger than that seen in 2017 – previously the biggest annual increase on record – when the UK industry saw a 23.2bn year-on-year bump in streaming plays (see below).

The BPI’s confirmation of the 2020 UK audio streaming numbers arrives amid a flurry of new stats from the trade org about the British market last year, based on Official Charts Company data.

There was rather less good news in these figures, according to MBW’s stat-crunching, on the matter of album sales.

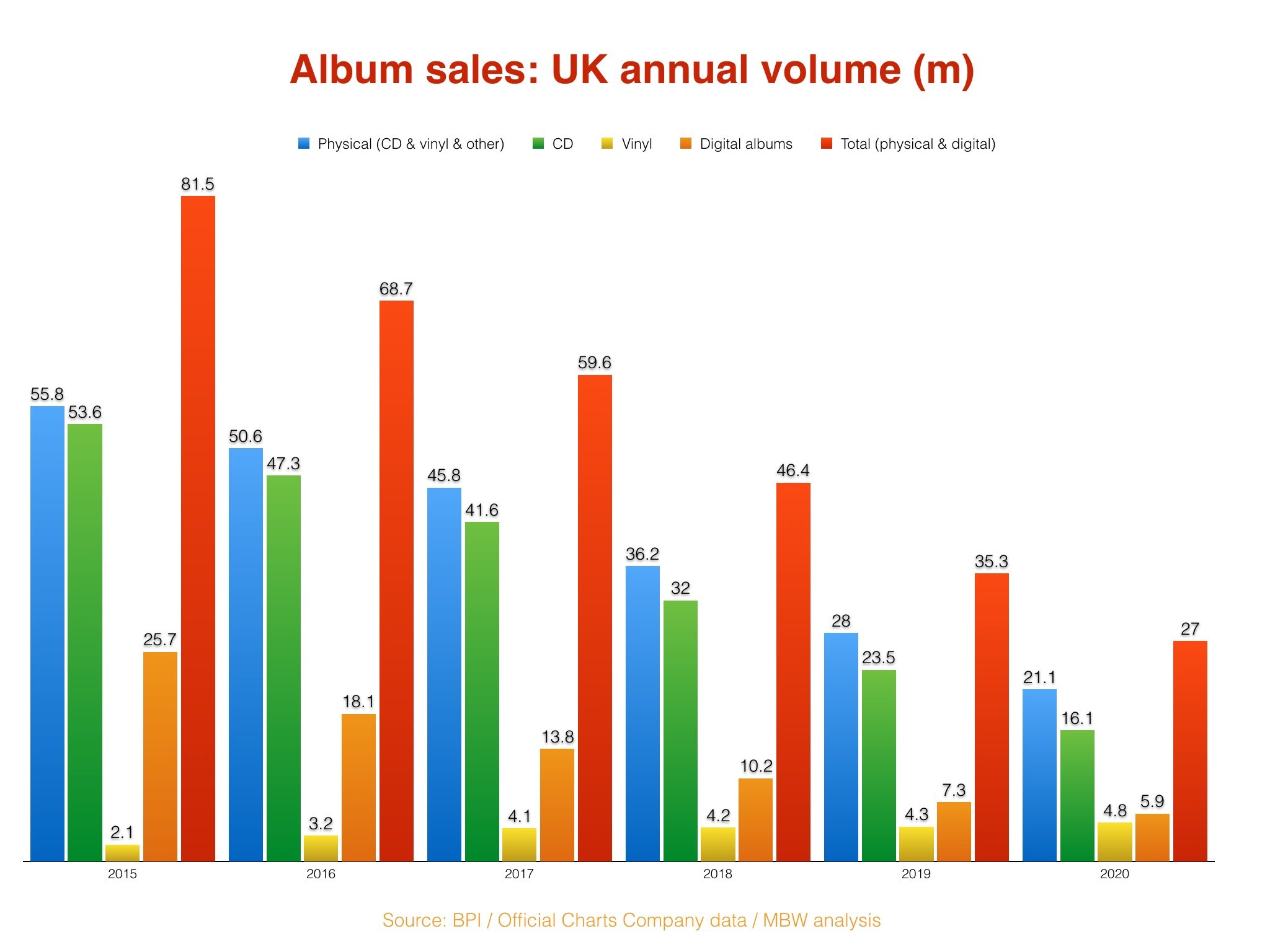

Total UK album sales (across physical and digital) fell 23.5% to 27m in 2020.

That was less than half the annual figure seen as recently as 2017 (59.6m), and less than a third of the size of the total album sales seen in 2015 (81.5m).

CD sales fared particularly badly in 2020, down by nearly a third year-on-year (-31.5%) to 16.1m.

In fact, annual CD sales in the UK were slashed in half within just two years from 2018 (32m) to 2020 (16.1m).

Back on the streaming tip, the BPI confirms that nearly 200 artists achieved over 100m streams in the UK during 2020.

The org suggests that this stat demonstrates how streaming “has made access to music easier for fans, but also increased competition for attention”.

The BPI said in a press release: “The top 10 streaming artists in 2020 each achieved over half a billion streams in the UK alone. But below them in the top 200 there were many artists achieving more than 200 million streams, while further down still, even artists ranking between 500th– 1,000th achieved between 43 million and 21 million UK streams. A million streams may sound a lot out of context, but 8,000 different acts now exceed this threshold [in the UK] annually.”

“Even at the lower end of streaming volume has surged, with more than six times as many artists achieving 100,000 streams as the equivalent number of sales in 2007.”

BPI statement

The BPI continued: “The market has become much more competitive, with many more artists able to access distribution and streaming platforms. Even at the lower end of streaming volume has surged, with more than six times as many artists achieving 100,000 streams as the equivalent number of sales in 2007.

“This means competition for consumer attention has intensified, requiring 24/7 fan engagement and marketing. And this is where labels are stepping up with £250m of [annual] A&R investment, helping British artists to continue to lead the world.”

On that note, Geoff Taylor, Chief Executive BPI, BRIT Awards & Mercury Prize, said: “Streaming means that there are many more artists active in the market than ever before. This is great news for fans, but means that it is harder than ever for artists to achieve success – so that continued support and investment from record labels in marketing and production is crucial.”

“Streaming means that there are many more artists active in the market than ever before. This is great news for fans, but means that it is harder than ever for artists to achieve success – so that continued support and investment from record labels in marketing and production is crucial.”

Geoff Taylor, BPI

He added: “The performance of recorded music in 2020 was remarkable, and reminds us how important music is to our country, even when our lives are disrupted. But any satisfaction we can take is tempered by the devastating impact of the pandemic on live music. Recorded music is only one element of artists’ incomes, and we renew our calls on government to support our culturally important venues, nightclubs and festivals until they can safely reopen.”

The UK’s biggest album in 2020 – in terms of consumer consumption across all formats – was Lewis Capaldi’s Divinely Uninspired To A Hellish Extent, which was originally released in 2019.

The UK’s second biggest album last year was Fine Line by Harry Styles (pictured), with Dua Lipa’s Future Nostalgia at No.3.