Will the global recorded music industry’s revenues finish 2020 flat, or even slightly up, on last year – despite the negative commercial effects of the global pandemic?

Over the past few weeks we’ve witnessed the recorded music arms of the two biggest majors (Universal and Sony) post modest YoY rises in half-year revenues; but in terms of Q2 alone, i.e. the three months to end of June, both companies saw revenues fall versus the same period of 2019.

These declines were caused by, amongst other pandemic-related hindrances, the closure of physical retail, the shrinking of Triple-A release schedules, and a reduction in public performance licensing income from shops, restaurants, bars, theaters etc.

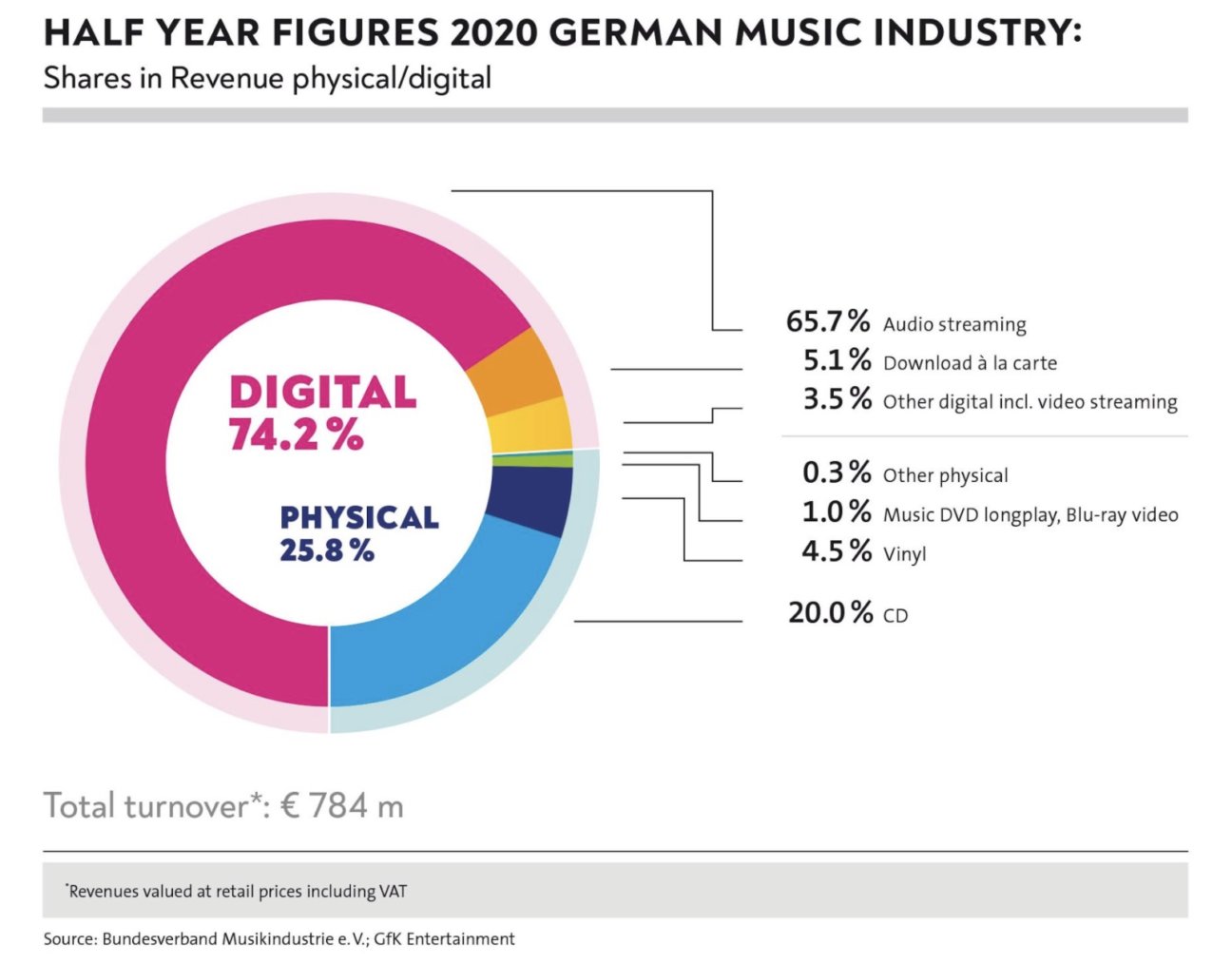

Today (August 20), brings some positive news arrives for the worldwide music business out of Germany, where industry-wide recorded music revenues rose 4.8% year-on-year in the first six months of 2020, up to €783.7m ($856m).

This 4.8% growth, unsurprisingly, was driven by audio streaming.

(Germany’s industry revenues, reported by the BVMI, are on a retail basis – covering the money handed over by German consumers for streaming services, downloads and physical music, in addition to advertising income from digital services.)

In the six months to end of June, audio streaming services like Spotify and Apple Music generated approximately €514.9m ($562m) in Germany, which the BVMI says was up 20.7% year-on-year.

This audio streaming haul made up 65.7% of Germany’s total recorded music retail revenues in the period.

The second biggest contributor to Germany’s industry in the six months was CD sales, with 20% of all recorded music revenues.

However, Germany’s CD sales were, predictably, down heavily YoY (-22.9%) in H1 2020, generating approximately €156.7m ($171m). That’s less than a third of the size of revenues pulled in by audio streaming in the same six months.

Combined with vinyl and other formats, Germany’s total physical music sales in H1 2020 hit €202.2m ($221m), down 18.6% year-on-year.

These stats represent a vastly transformed recorded music industry in Germany compared to that seen as recently as three years ago.

Germany is the world’s fourth biggest recorded music market (after the US, Japan and the UK), but has differed to some other billion-dollar territories in its enduring commitment to physical formats.

As recently as H1 2017, for example, BVMI stats show that physical formats (52.5%) still made up the majority of market revenues.

In the first half of this year, partly driven by conditions created by the pandemic, the share of physical formats fell to less than half this amount (25.8%), with audio streaming claiming more than two thirds of the pie (65.7%).

Elsewhere in the German market in the first half of this year, video streaming revenues grew 31.3%, says BVMI, but still only claimed a small market share of 3.3%.

Revenue from downloads continued to decline significantly (-22.5 %), with the format claiming a 5.1% market share. And vinyl as a standalone format claimed 4.5% of all industry revenues.

Dr. Florian Drücke, BVMI Chairman & CEO, celebrated the market growth in H1 2020, but had a warning for his member labels, suggesting that his organization’s “top priority” is now the implementation of the safe habor-zapping European Copyright Directive in Germany.

“The fact that the industry as a whole proved resilient in the corona crisis in the first half of 2020 is good news and a result of the successful digital strategy of the member companies in recent years,” said Drücke. “However, with a digital share of almost 75%, the literal implementation of the Copyright Directive in German law is now the top priority, because this is where the framework is set for the digital growth in the future.

“With a digital share of almost 75%, the literal implementation of the [European] Copyright Directive in German law is now the top priority, because this is where the framework is set for the digital growth in the future.”

Dr. Florian Drücke, BVMI

“The so-called discussion draft [of the Directive], which the BMJV recently presented, sends the really worrying and therefore unacceptable signal to the industry that a special German path is to be taken here, which neither reflects the Directive as it was originally intended nor the interests of the rights holders.”

Drücke continued: “It is, however, absolutely essential to place these positive figures in the overall music industry context, because the slight growth in our part of the industry must not distract from the extent of the crisis for the live sector – with the devastating effects for artists and all those who participate in the creation of value here.

“This can at best be slightly cushioned by the slight increase on the music sales side, but it is far from being compensated for. This is one of the reasons why we support the demands for state aid measures in a spirit of solidarity”.Music Business Worldwide